Understanding Student Debt Relief

Periodically, President Biden announces a new batch of student loan forgiveness. Each time, social media erupts with arguments against forgiveness, but for reasons that aren’t true.

It is fully constitutional

It is using laws already on the books from decades past

It is not saddling the rest of America with debt

Let’s walk through it:

Supreme Court

The Higher Education Relief Opportunities for Student Acts of 2003 allows the Secretary of Education to “waive or modify any statutory or regulatory provision” to protect borrowers affected by terrorist attacks, wars, or national emergencies. Trump had used this act to pause student loan repayments during the COVID-19 pandemic.

While President Biden continued that pause on loan payments when he took office, there were also ongoing discussions about loan forgiveness. It had been a major topic for Progressive Democrats during their campaigns, and Biden said he would look into what he could do.

The administration sought to use the HEROES Act to grant loan forgiveness of up to $10,000 for people earning less than $125,000 a year. The goal was to provide all of the relief in one fell swoop.

The Supreme Court ruled that such forgiveness was beyond the authority granted in the HEROES Act, which is why the incorrect claim that student loan forgiveness is unconstitutional is made.

Plan B

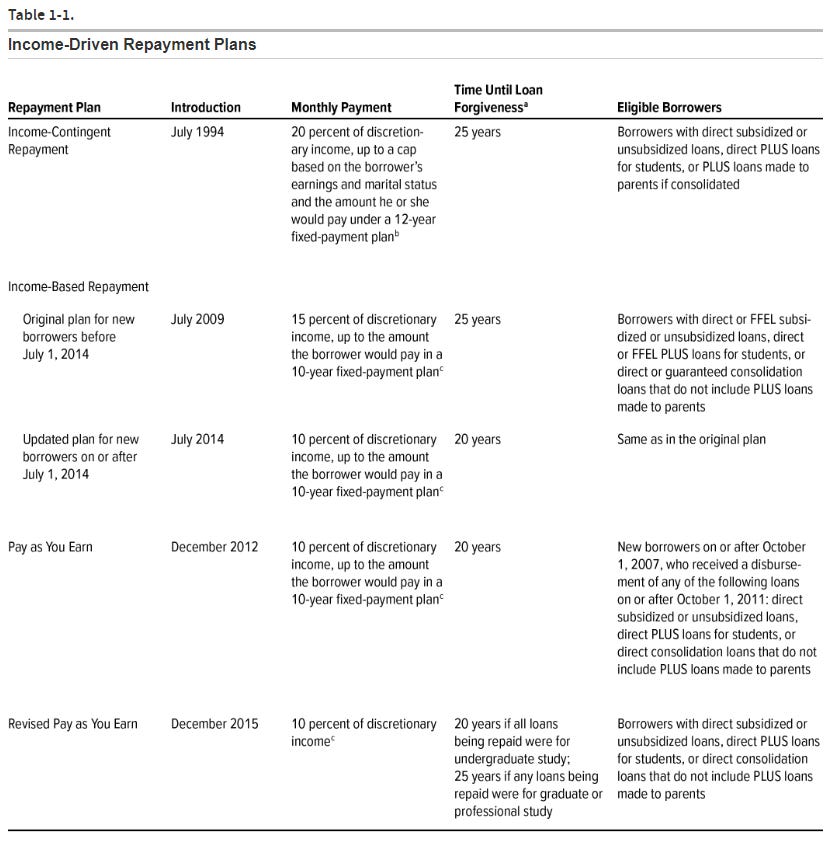

After the Supreme Court blocked forgiveness through the HEROES Act, the Biden administration switched to their secondary plan, which was to utilize the existing student loan forgiveness programs. This is why we see batches of student loan forgiveness. Each one targets a different program and sometimes different situations within those programs.

These various programs are based on income level and type of work, such as teaching, nursing, public service, and military service. Each program is meant to relieve those who have been paying off their loans for a long time, typically 20 years, but who still have a balance remaining.

The goal of these programs is to ensure that borrowers aren’t forever burdened with interest payments. Not only do people get stuck paying for decades, but some end up with a higher amount owed than they began with, even while making their payments on time.

The implementation of these programs has been plagued with issues. Despite over 2 million borrowers making payments for at least 20 years, only 32 people have received loan forgiveness through the Income-Driven Repayment program. The Public Service Loan Forgiveness program has managed to get relief to a still meager 7,000 people.

The Biden administration has worked around some of the mess bogging these programs down to get relief to those who have earned it. Borrowers who hadn’t received the forgiveness they were entitled to due to errors in paperwork, errors by the companies in charge of the programs, improper loan advice, or simply avoided the programs altogether due to their complexity and confusion.

Thanks to President Biden's work, millions of people have now received the loan forgiveness they were owed.

Student debt forgiveness laws have existed since the 1990s and have undergone several updates over the years. Anyone who claims that Biden is either ignoring Congress or breaking the Constitution simply isn’t aware of what avenues already exist and how broken they have been.

The Debt Is Not Transferred

The final misunderstanding is the belief that forgiveness is being burdened onto other Americans. It isn’t. The government is canceling the outstanding loan amounts, meaning no taxpayer money is being used. Instead, the government is forgoing future payments from these loan holders.

An argument can be made that the government losing out on future payments means less revenue, and therefore, it will cost taxpayers more money to pay for the federal budget.

This is a bit of a stretch because our national debt has shot up due to tax cuts for corporations and the wealthy. We can’t complain about lower future revenue at the same time as we’re intentionally reducing it.

It is also important to understand that the forgiveness is largely going to those who have paid off more than the amount they borrowed. It isn’t that the borrower is getting free money out of the deal. They are getting relief from the never-ending interest payments that they’ve been burdened by for over two decades.

We shouldn’t be planning our government spending around endlessly siphoning money from citizens for their whole lives just because they once needed money for college.

https://www.nclc.org/wp-content/uploads/2022/08/IB_IDR-1.pdf

https://www.cbo.gov/publication/56277

School Choice is a Failure

Giving parents the freedom to choose which school will best suit their child’s educational needs and providing those families with funds to put towards their choice. That is the standard line given by proponents of school choice. They go on to describe how helpless it feels as a parent to have your child locked into a failing school system when there may…